Interview

An Unprecedented CVC Development Program Realized by a Business Firm and JAFCO: Creating Business Together with Portfolio Companies

Jun. 26, 2025

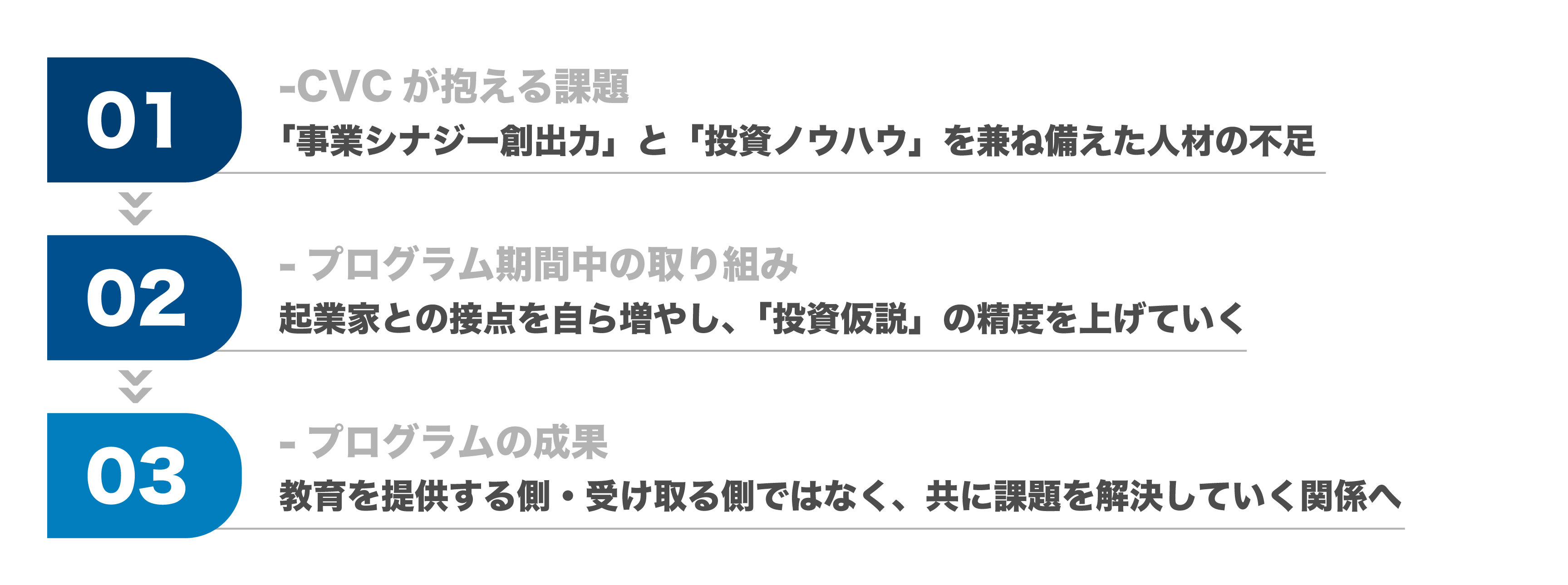

Corporate venture capital (CVC) is a form of investment operated by business corporations with the goal of generating business synergies with startups they invest in. To achieve this, knowledge and networks to create business synergies as well as know-how in startup investment are necessary. However, many CVCs face challenges due to a lack of these resources.

JAFCO has newly launched a development program targeting investment professionals within CVCs. Rather than the conventional method of being seconded to JAFCO to gain investment experience, this program allows participants to access training content online, delivered by JAFCO partners who are actively involved in startup investment.

This program was co-developed with Ono Pharmaceutical Co., Ltd., which manages its own CVC. This article presents the full picture of how this unprecedented initiative was carried out and what outcomes it achieved.

About Ono Pharmaceutical Co., Ltd.

Originally founded in 1717, Ono is a research and development-oriented pharmaceutical company based in Osaka which specializes in new drugs. The company focuses its R&D efforts on cancer, immunity, neurological, and specialty areas where there are unmet medical needs. In 2022, it established Ono Digital Health Investment, GK, a CVC aimed at investing in startups in the healthcare domain beyond pharmaceuticals.

Interview Participants

■ Ono Pharmaceutical Co., Ltd. / Ono Digital Health Investment, GK

Masakatsu Kobayashi - Manager, Strategic Alliance Section, Open Innovation Department, BX Promotion Division

Masanori Nishikori - Strategic Alliance Section, Open Innovation Department, BX Promotion Division

■JAFCO Group Co., Ltd.

Yutaro Saka – Partner, Investment Division

Takayuki Nishinaka – Principal, Business Development Division

Lack of Talent With Both Business Synergy Creation Ability and Investment Know-How

—First, please tell us about the background behind the establishment of Ono Digital Health Investment, Ono Pharmaceutical's CVC.

Kobayashi (Ono) Ono Pharmaceutical originally had a culture of open innovation to advance the creation of innovative drugs through collaboration with external partners. As a further step, we began investing in startups with the aim of creating businesses in healthcare areas beyond pharmaceuticals. To fully engage in investment activities, we established Ono Digital Health Investment in 2022.

Before this program, we had invested in five companies: one offering caregiving software based on scientific evidence, one providing AI-based medical imaging diagnostic support services, one developing biomaterial products for medical use, one developing online specific health guidance and SaMD for metabolic syndrome, and one offering at-home electrocardiogram testing services.

た。

—What challenges was Ono Digital Health Investment facing that led you to implement this program with JAFCO?

Kobayashi (Ono) Based on our investment activities so far, we wanted to accumulate more knowledge and experience to make better investment decisions. While some of our members had investment experience, many including myself had spent most of our careers at Ono Pharmaceutical. We felt that having more expertise would enable us to invest in better startups and fulfill our expected roles as a team.

We consulted various people, but the team at JAFCO especially took the time to listen to us sincerely. JAFCO is the first name that comes to mind when speaking of independent VCs in Japan, and they have a very well-structured internal system. The possibility of receiving support from various members was very reassuring.

—Are there many CVCs facing the same challenges that Mr. Kobayashi mentioned?

Nishinaka (JAFCO) Yes, that’s right. The objective of a CVC is business creation. It is important to work together with the parent company to generate business synergy with startups. In the case of people like Mr. Kobayashi and Mr. Nishikori who are internal, they have strong internal networks but little investment know-how. On the other hand, if someone with investment experience is hired from outside, they may have the know-how but lack the internal network, which makes it difficult to create synergy. I think this is a structural issue.

—I see. Could you tell us how this program was planned and implemented?

Nishinaka (JAFCO) Previously, when there was a need to nurture investment professionals, we would have them seconded to our company for a certain period to gain investment experience. However, with that method, it’s hard for the CVC side to balance their own duties, and for us as well, it was difficult to build a system that could accept people responsibly, making it burdensome for both sides. While talking with the team at Ono Pharmaceutical, we felt that a new kind of program, not involving secondment, was necessary.

This program was conducted entirely online, and it was designed to provide hands-on experience in evaluating startups and carrying out investments. It was implemented together with Mr. Saka, who’s a partner at JAFCO.

I don’t think a program like this to develop investment professionals exists in Japan, so rather than a relationship where we “provide” and they “receive” the program, we discussed creating it together on equal footing. I believe the fact that we both had this approach is what made the unprecedented program possible.

Kobayashi (Ono) At first, we were also considering the option of secondment, but we concluded that it would be difficult. So we discussed with everyone at JAFCO, including Mr. Saka and Mr. Nishinaka, how we could make this happen and explored what kind of program would be necessary for a CVC.

Mr. Saka is one of Japan’s leading investment professionals, deeply involved in his invested companies with extensive experience. We also wanted to take on challenges together with our investees and create new value in society, so we were confident that if Mr. Saka would be involved, it would be a highly valuable program.

Connecting With Entrepreneurs and Improving the Accuracy of Investment Hypotheses

—Mr. Nishikori, you represented Ono Pharmaceutical in this program. How did you come to participate?

Nishikori (Ono) I joined Ono Pharmaceutical as a new graduate and worked in departments such as sales, marketing, and medical affairs (promotion of clinical research planning).

Before joining this department, I had no involvement with startups, but in my previous departments, I had seen the high level of technology that startups possess add value to our company’s activities. That led to a strong interest in collaboration with startups, and when there was an internal call for applicants two years ago, I joined the team.

Mr. Kobayashi, our team leader, had already been preparing for this program with an eye to the future, and when it was officially launched, I felt it was perfect timing and decided to participate.

—So you joined the program with no prior experience in startup investment. What specifically did this program involve?

Nishinaka (JAFCO) The program was divided into Phase 1 and Phase 2. Phase 1 covered content necessary to conduct proper interviews with startup executives, such as understanding their business models and markets. Phase 2 focused on the know-how required to actually carry out investments, such as due diligence, negotiating terms, and investment contracts.

Between the two phases, we conducted regular one-on-one mentoring sessions for detailed support. The total program lasted about a year.

What we emphasized was not just delivering a program, but helping participants acquire practical know-how at a level where they could actually drive business creation as a CVC. During the program, Mr. Nishikori took on sourcing activities and interviews with startups as an investment professional for Ono Digital Health Investment.

Saka (JAFCO) During the first two to three weeks of Phase 1, we provided workshops to teach the essential knowledge and mindset needed as an investment professional. It covered the basics and core of startup investment, which are extremely important.

Nishikori (Ono) In the initial workshops, I learned from Mr. Saka about the key evaluation points and thinking processes that JAFCO emphasizes when assessing startups. It’s fundamental to clarify “whose problem and what kind of problem” the startup’s business solves, but through the workshop, I was reminded how important it is to have a very clear understanding of this.

—You mentioned that during the program, you also sourced and considered actual investment deals. What did you learn from that experience?

Nishikori (Ono) The most significant learning from Mr. Saka’s workshop was the investment hypothesis section. An investment hypothesis is a set of assumptions used to make investment decisions. I learned how to assess market conditions, product competitiveness, management, and other factors to determine a company’s strengths.

In addition, understanding what kind of problem the startup solves for whom became a key criterion for judging whether business synergy with our company could be expected. This was a valuable insight.

Saka (JAFCO) Startup investment differs from real estate or public stock investment, where there is plenty of past performance and quantitative data. Here, you have to make decisions based on unrealized information. And analyzing numbers alone will not give you the answer for a future that hasn't happened yet.

No one knows the right answer. That’s why the most important thing is to reach a point where, even if 99 out of 100 people disagree, you can confidently say, “I will invest in this company because...” That conviction must be supported by an investment hypothesis.

You need to think about how society and markets will change, what role the startup will play in that, and what kind of services it will offer to be needed by the world. But because times and information are constantly changing, and because each case is so specific, this kind of thinking can’t be taught like a textbook. So for Mr. Nishikori, we provided insights on how to form hypotheses in specific cases, helping him deepen his understanding.

—We heard that your first investment after the program was in TechDoctor, one of JAFCO’s portfolio companies. What challenges did you face leading up to this first investment?

Nishikori (Ono) The first hurdle was arranging interviews with startups. During the first four months of the program, I interviewed about 70 companies. Throughout the training period, I was constantly busy scheduling meetings and preparing for them in advance.

Saka (JAFCO) At JAFCO too, we think it’s important not to narrow your focus from the beginning, but to explore various business fields and actively look for technologies and services that you find interesting. This is necessary to strengthen your investment hypothesis. The more you interact with different businesses and ideas and add your own perspective, the more accurate your hypotheses become.

CVCs probably receive many startup introductions from various sources. That’s important too, but what’s even more important is for the investment professional to take initiative and go talk to entrepreneurs out of their own interest. This was one of the major themes of the program.

As Mr. Nishikori mentioned, setting up interviews and increasing the number is very hard. Keeping up that effort for several months with steady motivation might actually be the hardest part.

Nishikori (Ono) When meeting with startups, it’s important to have your own view on macro-level information such as social trends and developments. Without that axis, it becomes difficult to understand the startup’s business in depth, and the meetings lose value.

When I struggled to form investment hypotheses even after gathering information, I was advised to go back to the basics and ask, “Whose problem and what kind of problem is this solving?” By thoroughly repeating the process of examining the startup’s challenges from various perspectives and considering the rationale behind the hypothesis, I was able to build my ability to formulate investment hypotheses.

Nishinaka (JAFCO) Forming investment hypotheses requires a certain amount of information and experience, and to gain that information and experience, you need to build hypotheses and talk to many entrepreneurs. It’s a bit of a chicken-and-egg situation.

Kobayashi (Ono) It’s not always the case, but unlike VCs that pursue financial returns, CVCs have a business firm behind them. Startups may see CVCs as a valuable opportunity to connect with a parent company.

On the other hand, it’s also important for the business firm to consider what strategic returns they seek, and whether investment is the most appropriate means for both the startup and the company.

—What led to the investment decision in TechDoctor?

Nishikori (Ono) TechDoctor is a company aiming to realize AI-driven healthcare through the use of digital biomarkers (indicators obtained by collecting and analyzing data from devices such as wearables to visualize the presence of disease or changes from treatment).

Separate from this training program, I had actually received a request from our leader, Kobayashi, to prepare an internal report before we even considered the investment. The idea was to use it as a communication tool within the company, including with management, by laying out background information, why investment should be considered now, and how things might develop in the future, supported with specific examples.

One of the reports I wrote focused on digital biomarkers. At the time, I felt that digital biomarkers not only had potential to transform treatment, but also to address a variety of challenges in the healthcare field that had previously been out of reach. With this investment decision, I felt I was able to connect my personal experience with what I had been learning in the process of forming investment hypotheses.

Nishinaka (JAFCO) Before the investment, Mr. Nishikori had already prepared an internal report, and I was really impressed by the quality. It was highly persuasive, showing the outlook for the digital biomarker industry and logically deriving the need for investment. I felt he had put into practice both his experience at Ono Pharmaceutical and what Mr. Saka had conveyed, making the most of both.

Moving Beyond Teacher–Learner Relationship to Solve Problems Together

—After the investment in TechDoctor, a workshop was held to promote collaboration. Could you tell us about that?

Nishikori (Ono) Within Ono Digital Health Investment, which had conducted the investment review, there was a certain level of understanding of TechDoctor. However, I felt that mutual understanding between Ono Pharmaceutical, the parent company, and TechDoctor would be crucial for future development.

So, we organized a workshop with seven members from Ono Pharmaceutical, including those involved in new business development and CVC, and five members from TechDoctor, including the management team. The purpose was to “stand together at the starting line” as we worked toward future collaboration.

Nishinaka (JAFCO) When a business firm and a startup meet, each tends to put great effort into presenting their company and products in the best possible light, which often results in a situation where only the positives are emphasized.

But since new initiatives are inherently full of challenges, there should be opportunities to openly share those difficulties. Before exploring business ideas, both sides need to understand each other’s challenges and align perspectives. We created the workshop as a place for that kind of exchange.

Nishikori (Ono) Since the workshop, discussions with TechDoctor members have been happening almost weekly, and we are now moving forward in considering specific collaborations aimed at creating new businesses. The workshop greatly deepened mutual understanding between the two companies.

One of the biggest outcomes was the active communication that emerged, aimed at generating new value. Within Ono as well, expectations are growing across multiple departments that TechDoctor’s capabilities could be utilized in various ways, and internal exploration has already begun.

—Finally, could each of you share your overall reflections on this initiative?

Nishikori (Ono) This program gave us the opportunity to learn not only about the process leading up to investment execution but also about the full range of post-investment support that JAFCO actually puts into practice. I believe what I learned will not only contribute to my personal growth but also significantly enhance both the quality and breadth of our CVC activities. Going forward, I want to apply these learnings to further strengthen support for our portfolio startups, promote business co-creation, and create new value in the healthcare field.

Kobayashi (Ono) Ono Digital Health Investment may be a latecomer in CVC, but we want to make the most of the knowledge and expertise we gained through this program to further strengthen initiatives for co-creating businesses with our portfolio startups. By leveraging the experience and networks we have cultivated as a pharmaceutical company over many years, we aim to challenge ourselves to realize innovation in healthcare together with a wide range of partners and to contribute to society.

Saka (JAFCO) This was our first time running a program in this format, and it gave us a deep understanding of what CVC members are looking for. Since then, we have been continuously updating the content, making it easier to convey and easier for participants to share within their own companies. My hope is that through this program, more people will engage deeply with startups.

Nishinaka (JAFCO) The initial context was “venture capitalist training,” but what was truly significant was that it was not a one-way relationship of teaching and receiving. Instead, we worked together from the same perspective and with a shared sense of challenges. I believe this kind of relationship with business firms is a valuable asset both for JAFCO and for our portfolio startups. Thank you very much for giving us this opportunity.